![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!IXc-!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9f7142a0-6602-495d-ab65-0e4c98cc67d4_450x450.png)

![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!lBsj!,e_trim:10:white/e_trim:10:transparent/h_48,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F0e0f61bc-e3f5-4f03-9c6e-5ca5da1fa095_1848x352.png)

Signals Brief: CMS Shuts Down ETC—What's Next for Kidney Payments?

As CMS winds down mandatory models like ETC, it raises the question of whether private payers will take on a larger role in kidney care innovation—or if fewer structured incentives will slow progress

What Happened

The Trump administration’s Medicare Innovation Center (CMMI) will shut down eight alternative payment models (APMs) by the end of the year, citing a strategic shift in federal payment policy. The first four terminations were announced just hours after Axios’ scoop, adding to the growing uncertainty around the future of federal value-based care models.

The first four models ending early include Maryland Total Cost of Care, Primary Care First, Making Care Primary, and the ESRD Treatment Choices (ETC) Model—a mandatory program designed to increase home dialysis and transplant rates. In addition, two upcoming drug pricing models have been canceled, including the $2 Medicare Drug List and a model aimed at incentivizing confirmatory trials for accelerated approval drugs.

CMS says these terminations will save $750 million and that participating providers will receive transition guidance. But some of these models, including ETC, have not yet demonstrated meaningful improvements in health outcomes or Medicare spending, according to their latest evaluations. CMMI currently operates 23 models and receives $10 billion in mandatory funding every decade to develop and test new payment models. While it’s common for a new administration to end or modify payment projects early in its term, the constant back-and-forth makes it difficult for providers to fully commit to these experimental models—a tension that has played out across the VBC landscape.1

Why It Matters

The elimination of the ETC Model is a major shift in kidney policy. It was one of only two mandatory models in all of CMMI, covering ~31% of dialysis facilities and clinicians treating ESRD patients. The model was designed to increase home dialysis and transplant rates—longstanding goals of federal kidney health initiatives—but now it joins a growing list of canceled experiments that never had time to fully mature.

CMS insists this is not a retreat from value-based care, but rather a shift to align with its statutory obligation and strategic goals. Yet, with no clear replacement, the move leaves providers, payers, and patients in limbo. Kidney care has been one of the most targeted areas for value-based reform, with bipartisan support over multiple administrations— even catalyzed by Trump and then-HHS Secretary Azar in 2019. If these efforts are being wound down, what does that mean for the future of kidney payment reform?

This decision also comes at a time when Medicare Advantage (MA) enrollment among ESRD patients is rising, particularly after the 21st Century Cures Act expanded eligibility in 2021. While MA’s role in kidney care continues to grow, it remains unclear whether these payment model shifts signal a broader handoff to private payers or simply a change in CMS’s strategy for federal APMs.2

Background

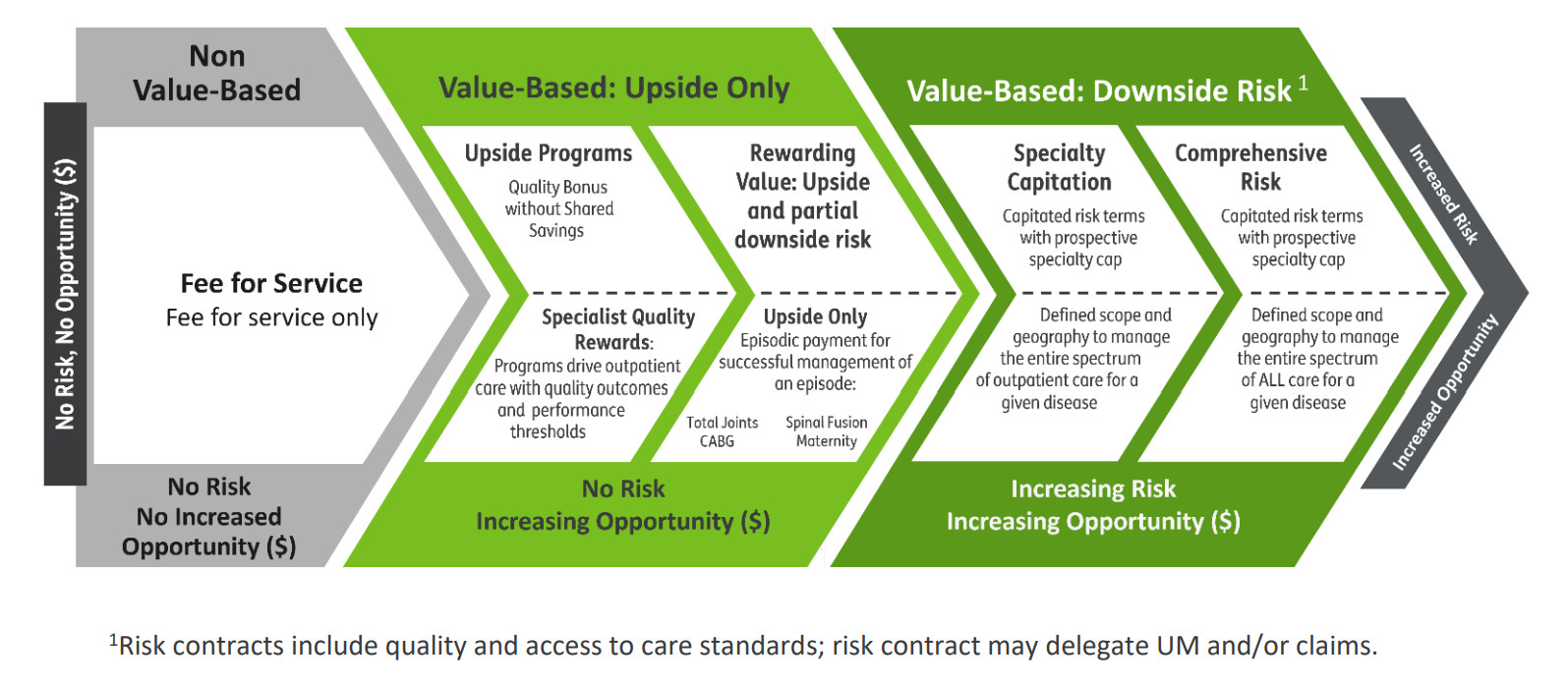

Since its creation under the Affordable Care Act (ACA) in 2010, CMMI has aimed to move Medicare away from traditional FFS payments in favor of alternative payment models (APMs) that reward efficiency, quality, and patient outcomes. But a long-standing debate has surrounded whether participation in these models should be voluntary or mandatory—a crucial distinction in how much impact they can actually drive.

Of 50+ models tested, only two have ever been mandatory, due to strong resistance from providers and policymakers. The pandemic further slowed momentum for pushing providers into risk-based models, and now, with CMS canceling the ETC Model, kidney care providers lose the only mandatory APM currently in place. For what it’s worth, the mandatory transplant (IOTA) model is currently scheduled to begin on July 1, 2025 and will include 103 kidney transplant programs.

Kidney-Focused Models

CMMI’s kidney-focused models have evolved over time, with a focus on care coordination, home dialysis adoption, and transplants. The two most recent models—ESRD Treatment Choices (ETC) and Kidney Care Choices (KCC)—were designed as successors to earlier payment reform efforts, but they took different approaches.3

The ETC Model was mandatory, requiring participation from 30% of the market to drive higher home dialysis and transplant rates. The KCC Model took an ACO-style approach, expanding beyond dialysis to include late-stage CKD patients and transplant recipients, aiming to slow progression, optimize dialysis starts, reduce costs, and improve patient outcomes. KCC also introduced new risk-sharing tracks, allowing participants to take on full financial risk (100%), a significant evolution from prior models.

While KCC’s first evaluation report showed early promise, ETC was cut before it could generate conclusive results. CMS’s latest evaluation noted that the model hadn’t yet demonstrated improvements in health outcomes or cost savings. With ETC now set for early termination, it raises a critical question: Will CMS continue supporting kidney-specific ACO models like KCC, or is this part of a broader retreat from mandatory risk-based models? On the other side of the table, how will the private sector respond— given their parallel trajectory of increasing risk and opportunity.

What’s Next

With the cancellation of the ETC Model, many in the kidney space are wondering what happens to KCC—and whether modifications are coming next. Both models were built as ACO-style frameworks for kidney payment reform, moving risk-based incentives upstream to improve early CKD management, dialysis starts, and transplant rates. While CMS has not yet announced changes to KCC, pulling the plug on ETC—the only other kidney-specific successor model—signals that federal payment policy is shifting.

This move is particularly striking given that Trump’s first term launched the Advancing American Kidney Health (AAKH) executive order in 2019, which set a bold 80% target for new ESRD patients to receive home dialysis or transplants by 2025. While aspirational, it spurred billions in investment around these kidney care models. The ETC Model was designed as a key lever to drive home dialysis and transplant growth, yet the U.S. has barely moved the needle—only 14% of patients are dialyzing at home today.

A recent JASN editorial response raised an uncomfortable question: Was the U.S. ever truly on track to hit these goals, or was denominator manipulation always the hidden lever? Given the choice between increasing available options (the numerator) or restricting access (the denominator), is a mandatory model a forcing function toward the path of least resistance?

Kate de Lisle of Leavitt Partners noted that CMS’s strategy is still taking shape, and further announcements may be delayed until after Dr. Oz’s confirmation as CMS Administrator. The administration says it wants to focus on “empowering people with information” and “driving choice and competition”, but it remains to be seen how that translates into policy.

As CMS reorganizes its APM portfolio, there are big unanswered questions for kidney care: What does this mean for value-based nephrology? What will KCC look like in its final two years? Is the future of risk-based kidney care simply shifting to Medicare Advantage and private payers? And, perhaps the biggest question of all: will chronic disease and cost cutting be major focus areas of the new administration— and if so, how will that eventually, inevitably reshape the kidney care landscape?

One day at a time. Keep exploring,

Thanks for being here and for all those who have reached out to share your thoughts and POVs. I know this is an evolving situation. Please share your thoughts below or join us in Slack to keep learning.

Discussion

How will nephrologists, dialysis providers, and transplant centers adapt if federal support for value-based kidney models diminishes?

Are Medicare Advantage plans ready to take on more risk for kidney patients, and what happens if CMS further scales back its role?

Should the kidney industry push for new payment models, or does the private sector offer a more stable alternative?

What does ETC’s termination mean for KCC? For IOTA? What would you like to see change (or stay the same) with these models?

How might this decision impact M&A activity in kidney care, particularly among value-based care providers?

Resources

In January 2024, the Lewin Group put together its Second Annual Evaluation Report of the ETC model. It’s a 158-page analysis of the ETC model and includes the summary graphic below on page 4.

ETC Findings at a Glance: “Through the first two years of the ETC Model, there was no difference in the growth in home dialysis between the ETC areas and the comparison group. Overall transplantation increased, but there was no significant increase on transplant waitlisting or living donor transplantation. There are no differences in Medicare spending, no worsening or improving of underlying disparities, and no unintended consequences. Given the challenges and the complexity of increasing home dialysis and transplant rates and the early stage of the model implementation, it is early to form conclusions about possible longer-term impacts of the model.” (cms.gov)

Nguyen KH, Oh EG, Meyers DJ, Kim D, Mehrotra R, Trivedi AN. Medicare Advantage Enrollment Among Beneficiaries With End-Stage Renal Disease in the First Year of the 21st Century Cures Act. JAMA. 2023 Mar 14;329(10):810-818. doi: 10.1001/jama.2023.1426. PMID: 36917063; PMCID: PMC10015314.

Kidney Care Choices (KCC) Model: KCC builds upon the Comprehensive End Stage Renal Disease (ESRD) Care (CEC) Model structure – in which dialysis facilities, nephrologists, and other health care providers form ESRD-focused accountable care organizations to manage care for beneficiaries with ESRD – by adding strong financial incentives for health care providers to manage the care for Medicare beneficiaries with chronic kidney disease (CKD) stages 4 and 5 and ESRD, to delay the onset of dialysis and to incentivize kidney transplantation. The model has four payment options: CMS Kidney Care First (KCF) Option, Comprehensive Kidney Care Contracting (CKCC) Graduated Option, CKCC Professional Option, and CKCC Global Option. (CMS.gov)