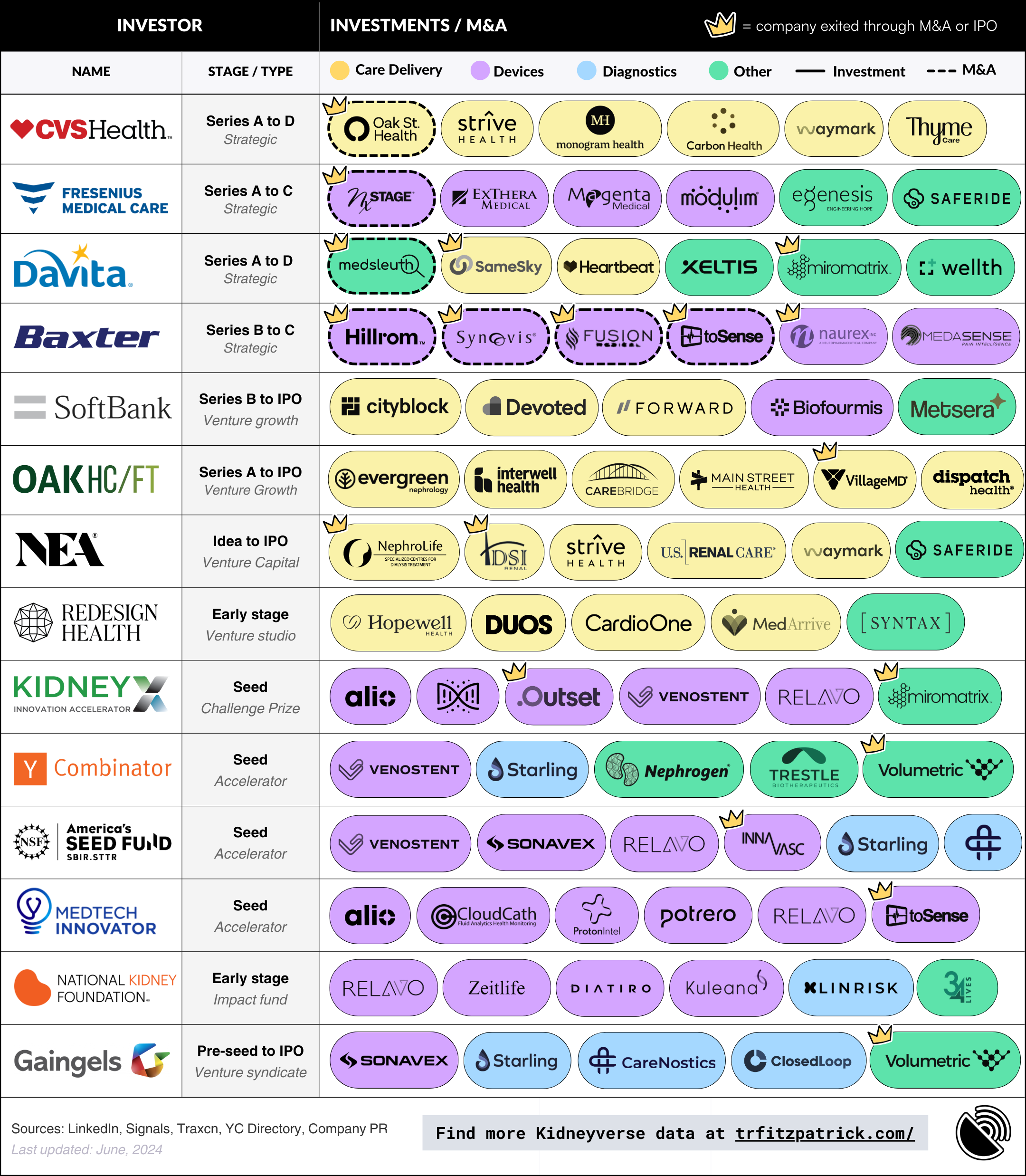

![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!IXc-!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9f7142a0-6602-495d-ab65-0e4c98cc67d4_450x450.png)

![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!lBsj!,e_trim:10:white/e_trim:10:transparent/h_48,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F0e0f61bc-e3f5-4f03-9c6e-5ca5da1fa095_1848x352.png)

Kidney Capital, Part 3: Top Underfunded Opportunities in Kidney Care

Sizing up the gaps that could define the next decade of kidney care progress

Welcome back to Kidney Capital, the series where we explore what gets funded in kidney care, and what does not. In Part 1, we looked at who’s writing checks across the Kidneyverse, from accelerators to strategics, and what sectors they’ve been betting on.1 In Part 2, we mapped the messy middle of capital formation: the gap between public dollars, early traction, and commercial scale.

Now in Part 3, we’re flipping the lens. Instead of tracking where capital has gone, we’re mapping where it hasn’t… yet.

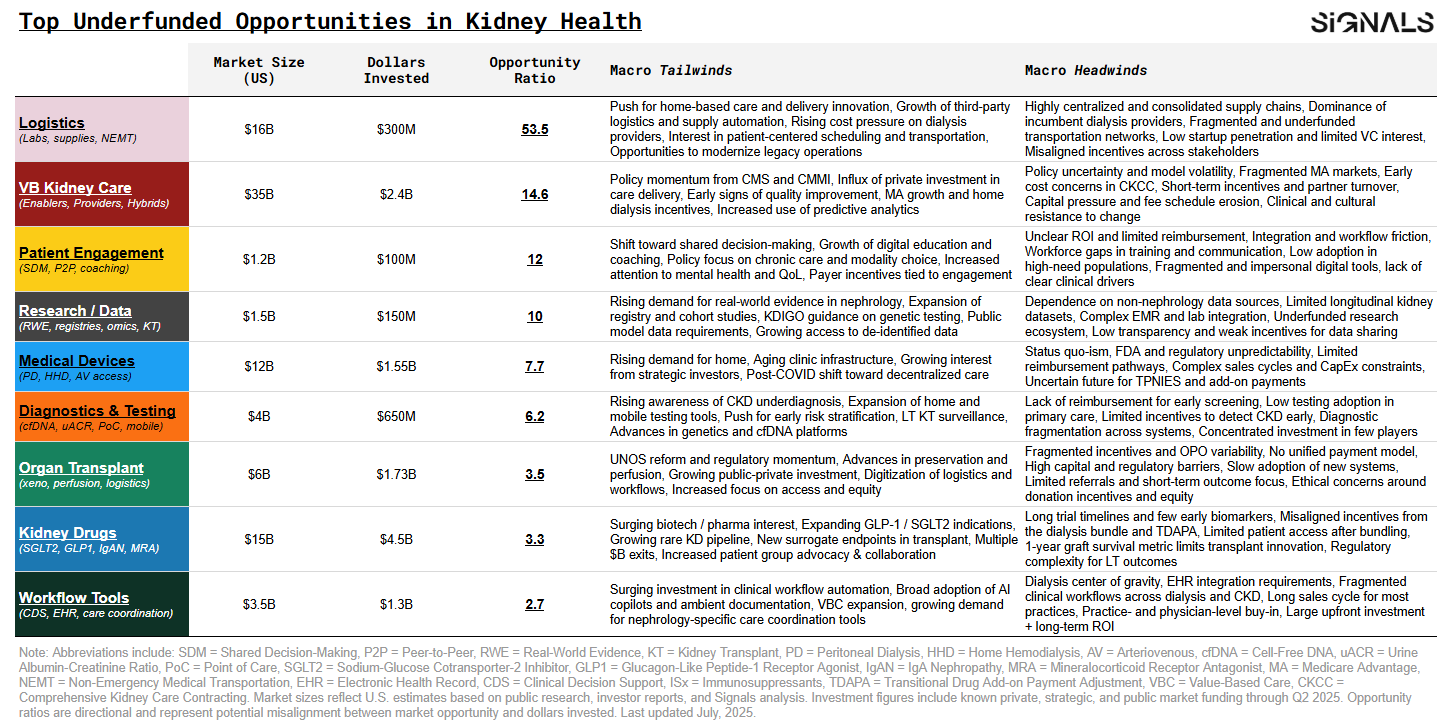

This chart highlights the top underfunded innovation categories in kidney care today—ranked by “opportunity ratio,” a simple metric comparing market size to total dollars invested. The higher the number, the greater the mismatch between potential impact and capital deployed. Some of the results won’t surprise you. Patient engagement, care coordination, and diagnostics have long been underfunded despite universal acknowledgment of their importance.2

But others might. Drug development across the kidney landscape appears to be entering a golden era of sorts, finally gaining steam after decades of slow progress. from single-agent ACE inhibitors in the early 1990s to today’s era of multidrug regimens. Workflow tools are riding an AI wave, but still underserved in nephrology settings. And transplant infrastructure, despite breakthrough headlines, remains starved of capital relative to its strategic and societal value.

What’s clear is this: the next decade of kidney innovation won’t be defined solely by what’s technically possible—it’ll be shaped by what gets funded.

Opportunity Areas

Logistics (Ratio: 53.3)

Logistics in kidney care includes the physical and operational infrastructure that supports dialysis delivery—labs, supplies, equipment servicing, transportation, home delivery, and waste management. The $16B U.S. market is largely controlled by incumbents like Fresenius, DaVita, and Quest, with deeply entrenched procurement relationships and limited transparency.3 Most innovation in this space has focused on iterative overlays or service optimization, rather than rethinking the system itself. Despite early hopes for widespread home dialysis adoption, in-center care still dominates. Notably, Fresenius is now investing in its high-volume hemodiafiltration (HVHDF) US rollout and aims to produce up to 20,000 5008X machines annually by 2030, alongside 100% control of consumables. This segment remains difficult to penetrate, but its size and potential transition with new delivery models make it one of the most overlooked opportunities out there.

Value-Based Kidney Care (OR: 14.6)

Value-based care continues to be one of the largest and most strategically important segments in kidney care. With a $35B+ market driven by Medicare Advantage, KCC, and public programs, the potential to reduce costs while shifting care upstream has many winners in theory— most of all, patients. A staggering $2.4B has been invested into platforms specifically providing (or enabling) VBC in nephrology. These groups bring enhanced capabilities (e.g. analytics, care coordination, risk adjustment) to practices to enable their transition to VBC, and increasingly share risk. While private capital (much of it private equity) is flowing into a concentrated group of companies, the policy landscape remains rocky, the model’s future uncertain, partner turnover happens more often than we hear about, and year-over-year physician FFS revenue erosion is squeezing delivery margins. Despite these headwinds, value-based kidney care continues its march ahead as new incentives, outcomes, and MA growth put an increasing number of patients in VB arrangements.4

Patient Engagement (OR: 12)

Patient engagement remains one of the most cited unmet needs in kidney care—and one of the most underfunded. Despite a $1.25B market opportunity across education, mental health, decision support, and behavior change, less than $100M has been invested in kidney-specific platforms. Adoption remains low among high-risk populations, and providers face real barriers around training, language access, and integration. Many tools are perceived as “nice-to-haves” rather than clinical essentials, and reimbursement remains scarce outside of MA and value-based programs. Patient navigation and peer-to-peer coaching—proven in oncology and transplant care—have demonstrated impact in kidney settings but are still not standard of care. This is a growing opportunity for payers and VBC orgs looking to meet equity and experience benchmarks through scalable, human-centered engagement models.

Research & Data (OR: 10)

Data and research tools power everything from registries and cohort studies to real-world evidence and discovery. Despite a nascent billion-dollar market opportunity, kidney-specific platforms have received less than $200 million in funding—most of it concentrated in diagnostics-adjacent players and a handful of AI/ML-as-a-service tools. Fragmented data systems, lack of longitudinal datasets, and poor incentives for sharing slow down innovation. Many platforms now depend on partnerships with HIEs and health systems, with the latter slow to engage or simply focused elsewhere. Even when high-quality tools are available, many provider groups and care teams lack the expertise to fully leverage them—limiting impact and scale (see VB trend). Still, demand for kidney-specific RWE is increasing from payers, regulators, and biotech, so we may see meaningful TAM expansion here—driven by both biotech demand and new investment. This segment is poised to expand significantly as tailwinds from drug development and platform biotech fuel demand for high-quality cardiorenal and metabolic data.

Medical Devices (OR: 7.7)

Kidney devices—including dialysis machines, vascular access tools, and extracorporeal support systems—represent a $12B+ U.S. market. While high-profile companies like Outset and Quanta have raised substantial funding, total investment in the category is still under $1.6B—disproportionate to the complexity and scale of the market. FDA approval pathways are slow and expensive, and long capital cycles limit investor participation. Even with TPNIES, devices face the eventual squeeze of being bundled under a fixed payment model, which limits upside and slows adoption. Still, demand for simplified systems, portable machines, and automated access tools continues to grow. This remains a capital-intensive but essential area, with opportunity expanding as infrastructure ages and care shifts outside the clinic.

Diagnostics & Testing (OR: 6.2)

Diagnostics sits at the center of early detection, yet it remains structurally undervalued. The $4B U.S. market spans screening, risk stratification, transplant monitoring, and emerging biomarker platforms. But only ~$650M has been invested to date, much of it concentrated in just a few companies like Renalytix, Natera, and Healthy.io. Screening still lacks reimbursement support, especially for early-stage CKD, and diagnostic innovation often faces slow adoption in primary care. That said, cfDNA platforms, genetic testing, and point-of-care testing are all advancing—and payer attention is shifting with new guideline support. This segment is poised to grow as early detection becomes a focus of both top-down public policy and commercial payer / group health plan cost containment strategies.

Transplant Access (OR: 3.5)

Transplant access spans organ donation, preservation, logistics, xenotransplant, and transplant-specific workflow tools—yet still receives limited funding. With an estimated $6B U.S. market and only ~$1.7B in capital raised to date, investment has been largely confined to device-heavy companies like TransMedics and Paragonix, and a few major bets on xenotransplantation like eGenesis. The lack of a unified payment model, fragmented hospital incentives, and limited referral patterns slow adoption. Ethical considerations around incentives and equity also remain a challenge. However, federal reform efforts, new preservation tools, and increased transplant center attention are shifting the conversation. This opportunity is expanding as technology, policy, and public pressure converge to modernize transplant logistics and access.

Kidney Drugs (OR: 3.3)

After decades of underinvestment, kidney drug development is finally picking up momentum. The $15B U.S. market includes a mix of broad-label drugs (like GLP-1s and SGLT2s), burgeoning disease-specific treatments (IgAN, FSGS, APOL1), and transplant-related immunosuppressants. Recent exits like Chinook, Travere, HI-Bio, and Regulus have helped validate the space, alongside a growing pipeline of early-stage biotechs (Purespring, Judo, Borealis, Renasant) targeting podocyte biology, gene therapy, and rare kidney conditions. Still, structural headwinds persist: limited biomarkers and endpoints, complex trial design, and reimbursement barriers tied to the ESRD bundle TDAPA. Transplant drug innovation is also hindered by the narrow focus on one-year graft survival rather than long-term function or quality of life. This market is expanding as biotech and platform investors look to replicate recent wins and unlock the next wave of kidney therapeutics.

Workflow Tools (OR: 2.7)

Workflow tools for kidney care are finally getting attention, boosted by AI copilots, documentation tech, and VBC data requirements. The $3.5B market includes EHR plugins, referral tracking, CDS tools, and care coordination platforms, but less than $1.3B has been invested to date—most of it in horizontal players like Abridge, Nabla, and DeepScribe. Integration with nephrology workflows remains a challenge, especially in small practices and dialysis environments. Hospitals and integrated health systems appear to be driving much of this growth. Beyond broader admin and RCM-driven fervor, ROI can be hard to prove, and nephrology-specific features are often an afterthought. Still, new partnerships and purpose-built tools are emerging.

With AI momentum and CKCC infrastructure maturing, workflow tools represent one of the fastest-expanding investment opportunities in kidney care.

What’s next

These ten categories represent more than a list—they reflect the structural gaps, market misalignments, and overlooked opportunities that stand to reshape kidney health. While some are underfunded because they’re hard to solve technically, others remain ignored because they’re fragmented, misunderstood, or misaligned with current incentives. That’s exactly where the next generation of builders, investors, and operators can make a difference.

To support that effort, we’ve launched the new Signals Directory, a global index of over 90 companies (and growing) across the kidney innovation lifecycle—from idea to IPO. It’s designed to help you explore who’s building what, and where momentum is forming across these underfunded areas.

And if you haven’t already, we’d love your input in our Top Unmet Needs in Kidney Care Survey, where we’re gathering frontline and field-wide perspectives on what problems matter most—and where solutions are still falling short. So far, 45% of survey respondents are patients or care partners, and 30% of respondents say “early CKD screening and detection” is our top priority area. What do you think?

Let’s keep mapping the gaps—and building what’s next.

Methodology Note: This analysis combines market size estimates and capital investment data across 10 innovation segments in kidney care. Market sizes reflect U.S. estimates based on public research, payer data, company reports, and Signals modeling. Investment totals include venture, private equity, and strategic funding for companies with a kidney-relevant product or service, with a focus on those founded or actively fundraising in the last 10 years.

Opportunity ratios are directional indicators only, intended to highlight potential misalignment between market need and capital flow. Some categories (like transplant access or workflow tools) are underdeveloped markets with few traditional benchmarks, so we welcome suggestions to improve how we structure and update this view. This is our first full landscape of underfunded opportunities in the Kidneyverse—and we’ll keep refining it with your feedback.

*Inspired by the world class team at Fifty Years. Check out their Progress Index here.

Logistics Market Sizing: The estimated $16B U.S. dialysis logistics market includes the full scope of infrastructure supporting in-center and home dialysis delivery. This encompasses consumables and supplies, lab testing, home delivery and fulfillment, non-emergency medical transportation (NEMT), waste management, and equipment servicing. While much of this market is dominated by a few incumbents, we include it in the total addressable market to reflect the operational scale and modernization required to support future care models. This also accounts for new infrastructure shifts, including the HVHDF rollout, PD supply chain resilience, and POC dialysate generation. Although this is a highly consolidated and procurement-heavy segment, we believe its modernization is critical—and historically underfunded—making it one of the most overlooked infrastructure opportunities in kidney care.

VB Kidney Care Market Sizing: This estimate is based on CMS and USRDS data showing ~$120B in annual U.S. healthcare spending for patients with CKD and ESRD. That includes ~$51B for ESRD and an additional ~$70B+ for CKD stages 3–5, much of it driven by hospitalizations and late-stage complications. A growing number of value-based kidney care companies report managing more than $19B in annual medical spend, or roughly 15–20% of total CKD/ESRD costs. We estimate the addressable value-based care market at ~$35B based on the portion of total spend that is actively being targeted for reduction through care coordination, risk contracting, and earlier intervention. This includes costs managed through CKCC, Medicare Advantage, ACO REACH, and commercial VBC arrangements. As more lives shift into risk-bearing models and MA enrollment grows, this market is expected to expand.