![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!IXc-!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9f7142a0-6602-495d-ab65-0e4c98cc67d4_450x450.png)

![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!lBsj!,e_trim:10:white/e_trim:10:transparent/h_48,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F0e0f61bc-e3f5-4f03-9c6e-5ca5da1fa095_1848x352.png)

Part 3: Following the Spend

Why kidney care became the proving ground for healthcare's trillion-dollar accountability transition.

In Part 1, we argued that the kidney is medicine’s early warning signal. In Part 2, we explored how many of healthcare’s largest opportunities exist in the spaces between specialties. Both ideas point toward the same conclusion: healthcare is slowly moving toward a system where payment is tied more directly to outcomes, not just services delivered. That shift matters because fee-for-service still drives much of specialty care revenue, even when better health outcomes require coordination across conditions, clinicians, and settings. Kidney care is emerging as one of the first places where this transition can be measured, managed, and scaled to reduce overall spending.

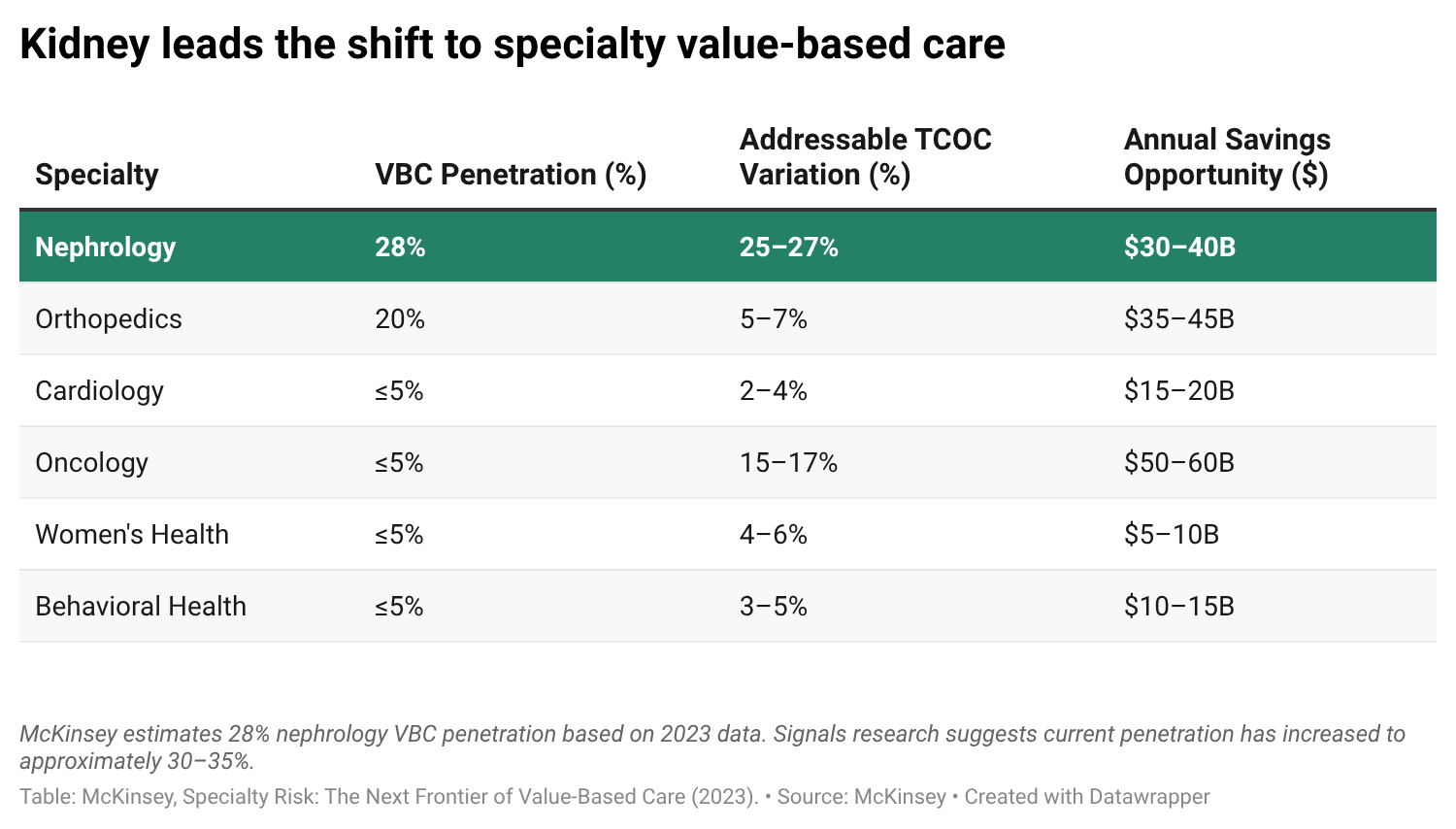

The backdrop is straightforward. Healthcare spending continues to climb, but the fastest growth is increasingly concentrated in specialty care. Six specialties—orthopedics, oncology, cardiology, women’s health, behavioral health, and nephrology—now account for 38% of Medicare and commercial medical spending and touch patients responsible for more than two-thirds of total healthcare expenditures. Between 2020 and 2023, spending across those specialties grew 35% faster than the rest of the market.

That matters because the payment model shapes the care model. In fee-for-service, specialty care is largely paid based on visits, tests, procedures, and activity. In value-based care, payment begins to shift toward outcomes: keeping people healthier, avoiding preventable complications, and managing total cost of care. The hard part is that not every specialist is moving through the same model at the same time: a nephrologist may be accountable for a patient’s total cost of care while another specialist treating the same patient is still paid primarily through services and procedures.

Primary care has already moved much further in that direction, with more than half of Medicare beneficiaries now receiving care through some form of value-based arrangement. Specialty care remains earlier in the transition. McKinsey estimated that 28% of nephrology patient lives were managed under risk-bearing value-based contracts in 2023, compared with roughly 20% in orthopedics and 5% or less across several other high-spend specialties. Even at those levels, nephrology stood out as the clear leader among specialty categories. That leadership position is one reason kidney care has become an important proving ground for what accountable specialty care can achieve, especially as more kidney disease is identified and managed earlier in primary care.

What we’re seeing

Observation 1: The accountability gap in kidney care is closing faster than most investors realize. Since those 2023 estimates were published, value-based care adoption in nephrology has continued to expand. Based on Signals research, we estimate that approximately 30-35% of kidney patients are now managed under total cost of care arrangements, where organizations take responsibility for the broader cost and quality of care over time. CMS has made specialty value-based care expansion a priority, and new payment models are pulling more nephrology lives into risk-bearing structures. The infrastructure to manage those lives, including companies like Monogram, Strive, and Somatus, has absorbed nearly $1.6 billion in capital. That investment has demonstrated what is possible, while also surfacing where the hard problems remain: earlier identification, better monitoring, provider-level support, and more scalable patient-level support across multiple conditions.

Observation 2: The $608B combined cardio-kidney total cost of care represents one of the largest addressable pools in specialty medicine. Cardiology represents roughly $467 billion in annual total cost of care, while nephrology represents another $141 billion. These are often treated as separate markets, but they are frequently the same patient population viewed from different clinical entry points. That creates real friction in today’s payment system. A nephrologist may be working under a total-cost-of-care model, while the cardiologist managing the same patient is still paid largely through fee-for-service. One part of the system is rewarded for preventing avoidable complications, while another is still paid around visits, tests, and procedures. Cardio-kidney-metabolic disease is already converging clinically. The payment model has not fully caught up. The organizations that figure out how to manage that risk under a more connected model are building infrastructure for one of the largest accountable spend pools in American healthcare.

Observation 3: The investment thesis follows the spend, not the science. Nearly $10 billion has been deployed into platforms managing kidney and broader cardiometabolic populations at scale, and exits are beginning to emerge. Two digital health IPOs in 2025 reinforce the point: when companies can manage large populations, align with reimbursement, and show a path to durable outcomes, the market pays attention.1 As more specialty care moves into risk-bearing arrangements, the hard problems shift into execution: earlier diagnosis, continuous monitoring, patient engagement, AI-enabled workflows, and care delivery infrastructure. For early-stage investors, the opportunity is to build the enabling companies that help accountable platforms perform.

Where capital goes next

Kidney care has already done much of the hard work. Over the past decade, the field has served as a testing ground for new payment models, care delivery approaches, and accountability structures. Along the way, it has built infrastructure, attracted capital, and demonstrated what coordinated care can achieve at scale. Many of the same forces are now beginning to reach the rest of specialty medicine.

For investors, the opportunity increasingly lies in the enabling layer: the diagnostics, data infrastructure, AI tools, monitoring platforms, and workflow systems that make accountable care possible. The trillion-dollar shift we described in Part 1 is becoming market structure. The organizations building that foundation will help shape how the next decade of healthcare is delivered.

This series started with a simple observation: the kidney is an early signal for where medicine is heading. Over the coming months, we will continue exploring that idea alongside the founders, clinicians, researchers, operators, and industry leaders building the future of kidney and cardiometabolic care.

If you are building, investing, researching, or working on these challenges, we would love to hear from you.

Janis Naeve and Tim Fitzpatrick are Co-Founding Partners of Bright Frontier Capital, a new thesis-driven venture fund designed to shape the future of kidney and cardiometabolic health.

| A guest post by

|