![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!IXc-!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9f7142a0-6602-495d-ab65-0e4c98cc67d4_450x450.png)

![Signals From [Space]](https://substackcdn.com/image/fetch/$s_!lBsj!,e_trim:10:white/e_trim:10:transparent/h_48,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F0e0f61bc-e3f5-4f03-9c6e-5ca5da1fa095_1848x352.png)

What I’m celebrating this Kidney Month

Clinical practice, primary care, and payment models are building a new foundation for upstream kidney care. There is still work to be done.

Eight months ago, I published Five Charts That Explain the Current State of Kidney Care. It was an attempt to paint a clear picture of where the kidney world stood at that moment. As you may remember, the story was mixed. Real progress in some areas, stubborn inertia in others, especially early screening, home dialysis, and living donation.

Today kicks off Kidney Month. The burden of kidney disease remains enormous, and hundreds of millions of people still do not know they have it. But as I look across therapeutics, value-based care, primary care integration, and federal payment policy, the center of gravity feels different. The dialysis-centric story is no longer the only one shaping the conversation. Kidney care is being pulled upstream, earlier in the disease journey, and more tightly into cardiometabolic strategy. It’s early, but the signs are there.

We see it in prescribing patterns. We see it in risk-bearing contracts. We see it in how health systems and primary care groups are beginning to think about CKM populations as a risk profile rather than a collection of siloed diagnoses scattered across the medical record. Yes, it’s early innings, but the question is no longer whether kidney disease matters to the broader system. It is shifting to how quickly the system can reorganize around that reality, and who will lead the charge.

So this Kidney Month, I want to highlight four areas that give me reason for optimism. Not because the story is finished. It is not. But because the step-by-step direction of travel from here is already clearer than it was this time last year.

What’s Inside

Kidney moves upstream into CKM strategy

Risk-bearing care scales beyond nephrology

Primary care becomes the leverage point

Federal models continue to iterate

#1

First, the kidney is now at the center of cardio-metabolic care. For years, chronic kidney disease sat as an afterthought, downstream of diabetes, heart disease, and obesity. That dynamic has shifted considerably, with recent examples from the Super Bowl and the American Heart Association’s CKM Initiative reinforcing the message. But the shift is most visible in medication management. Considering most adults with CKD stages 3 to 5 are still more likely to die than progress to kidney failure, any movement toward earlier detection and treatment is meaningful.1

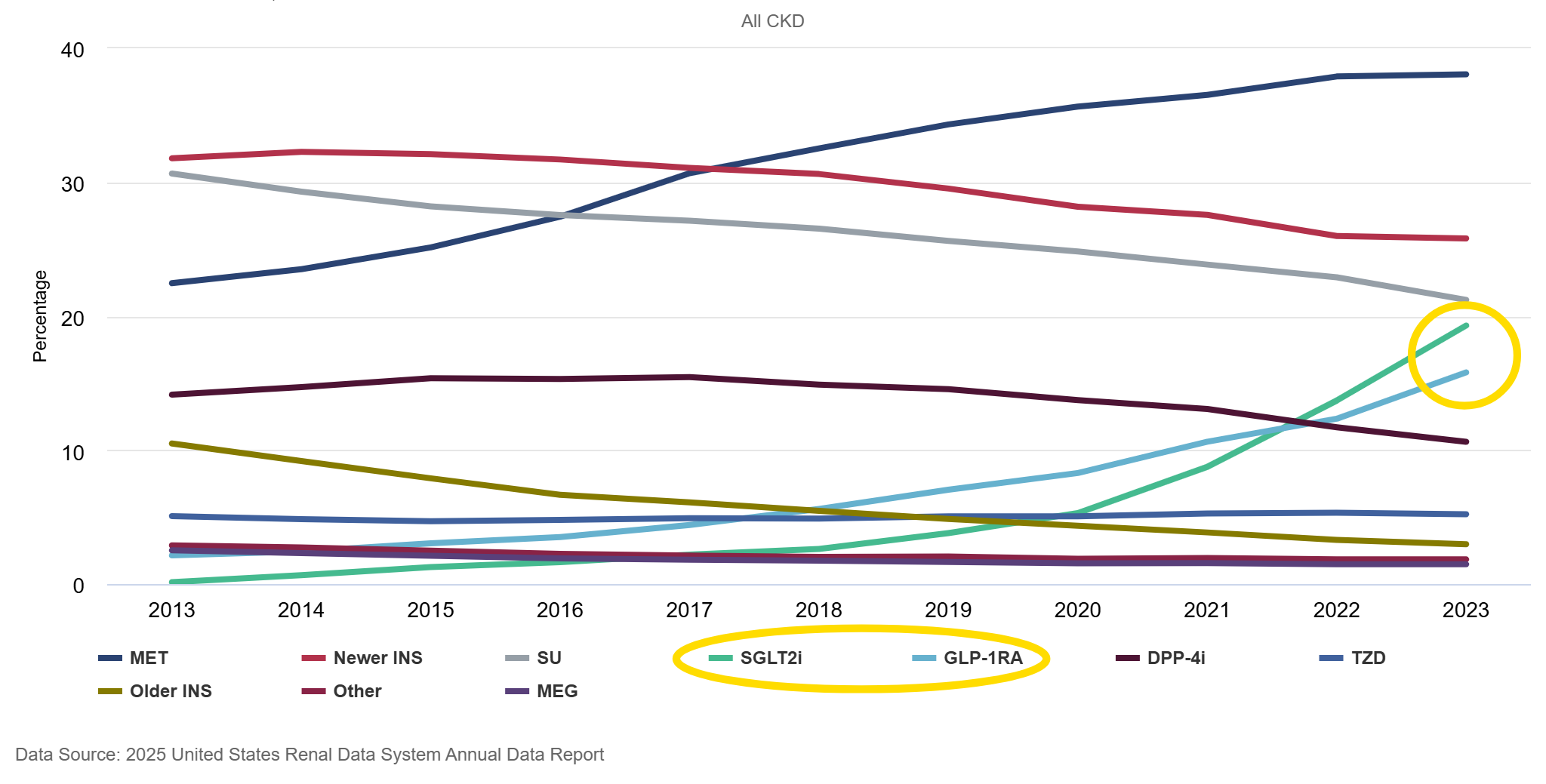

The 2025 USRDS Annual Data Report shows how prescribing patterns have evolved over the last decade.2 While traditional diabetes drugs have steadily declined, SGLT2 inhibitors and GLP-1 receptor agonists have accelerated since 2018. Nearly one in five Medicare beneficiaries with CKD and diabetes were receiving an SGLT2 inhibitor in 2023, and uptake was even higher among those who also had heart failure. GLP-1 use has followed a similar upward trajectory. Even among patients with stage 4 and 5 CKD, these newer classes are increasingly part of the treatment mix.

Figure: Percentage of older adult Medicare FFS beneficiaries with CKD and type 2 diabetes receiving diabetes medications, 2013-2023

These trends reflect more than incremental changes in diabetes care. They track closely with major cardiovascular and renal outcomes trials that established SGLT2 inhibitors and GLP-1 receptor agonists as organ-protective therapies.3 Clinical guidelines have incorporated those findings across specialties. The ADA and KDIGO emphasize early use in high-risk populations. The AHA now includes kidney function in its updated cardiovascular risk algorithm. Kidney endpoints are embedded in cardiovascular trials, and cardiovascular outcomes are central to renal studies. The therapeutic goal has shifted from glucose control alone to preservation of heart and kidney function across a connected cardio-kidney-metabolic axis.4

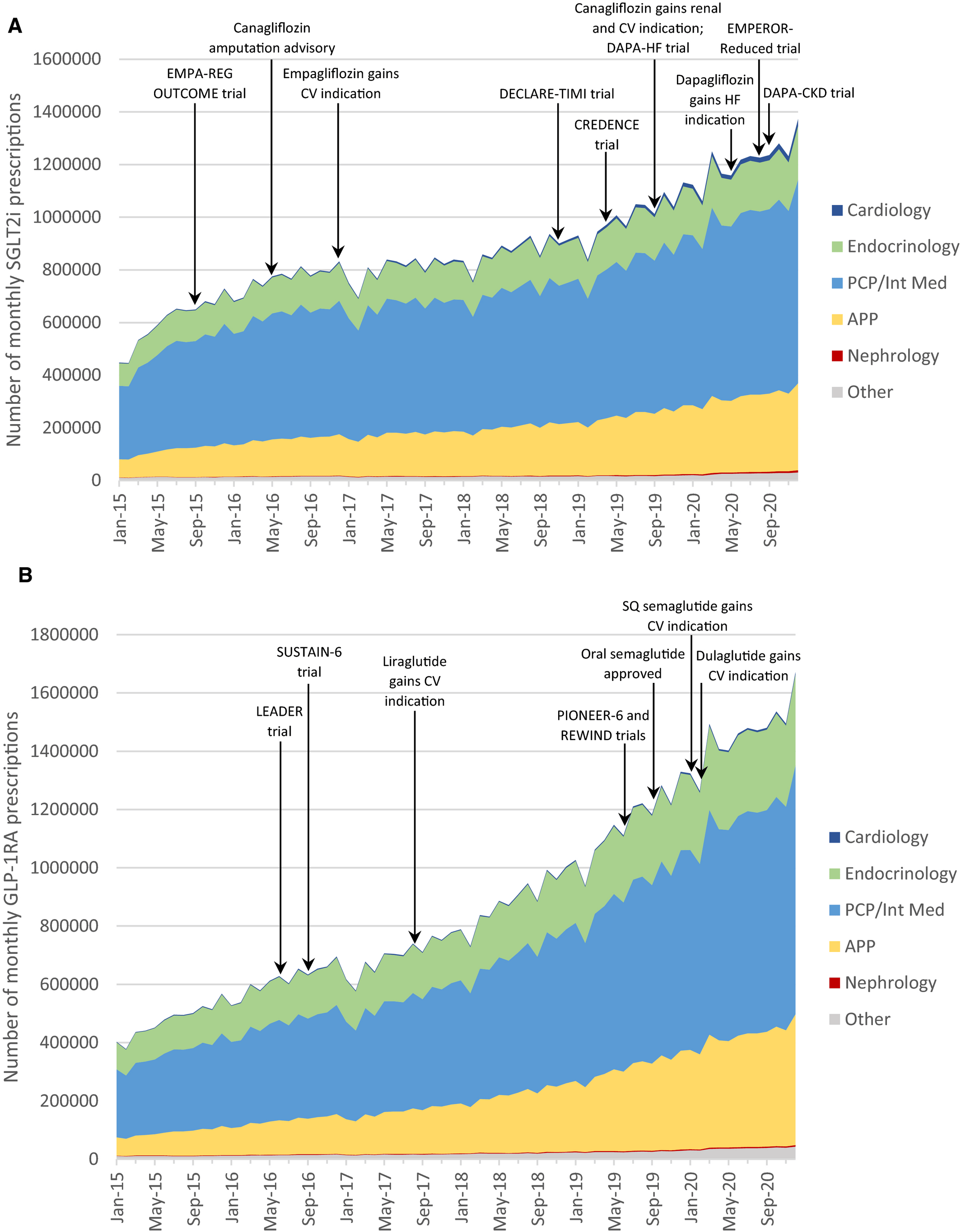

But who is actually writing these prescriptions? National prescribing data show that cardiology, primary care, and endocrinology account for the vast majority of SGLT2 and GLP-1 use, with nephrology representing only a small fraction of overall volume (see below).5 The inflection in prescribing aligns closely with major outcome trials and subsequent label expansions (here, here, and here). Kidney protection is being absorbed into mainstream cardiometabolic practice rather than remaining siloed within nephrology.6

Figure: (A) SGLT2 and (B) GLP‐1 use across clinician specialties

Adoption remains uneven. Patients with CKD who do not also carry diagnoses of diabetes or heart failure still have very low exposure to these agents. That’s important because many adults with advanced CKD do not see a kidney doctor. In 2023, only 41% of adults with Stage 5 CKD had a nephrology visit. But the direction is clear. Kidney preservation is no longer confined to specialty clinics. It is increasingly part of routine risk management in primary care and cardiology.

When cardiologists, endocrinologists, and primary care physicians are actively prescribing therapies that slow kidney decline, responsibility for CKD no longer sits with one specialty. That shared ownership is foundational to the integrated risk models now expanding across the country, especially as models differ in terms of who ultimately manages the outcomes and costs of that care.

#2

Second, integrated care is scaling through a specialty lens. The growth in kidney value-based care over the past several years is significant. In our latest review of the landscape, ten leading kidney-focused value-based organizations collectively manage more than 1.5 million patient lives and nearly 40 billion dollars in annual managed medical spend. That figure has roughly doubled from prior updates and now represents about 20 percent of fee-for-service Medicare spending across CKD and ESRD populations.

By our count, the number of lives under management has grown by nearly 50 percent in just the past year. Today, close to one-third of kidney disease patients are cared for within some form of value-based arrangement. Contract design varies greatly, but the scale alone is notable. Kidney care, long viewed as fragmented and reactive, is increasingly being managed under structures that hold organizations accountable for total cost of care. The financial risk is shifting from public to private payers; and further, from larger payers to specialized risk managers in the form of these VB kidney care entities (and not just in nephrology).

Figure: Ten companies manage ~1.5M patients and $37B in annualized medical spend across value-based nephrology models

Equally important is how these organizations are evolving. The largest players, including Somatus at roughly 500,000 lives, Panoramic at 330,000, Monogram at 200,000, and both Strive and Interwell at approximately 145,000 each, are no longer operating as kidney-only entities. Several have expanded aggressively into cardiology and broader multi-chronic populations. The top three now account for roughly two-thirds of total lives under management, and the mix increasingly reflects patients with overlapping heart failure and metabolic disease.

The financial layer reinforces this integration. Among providers reporting this data, estimated managed spend per patient ranges from roughly $15,000 to $75,000 annually, with an average near $33,000. That range reflects differences in acuity and contract structure, but it also illustrates the economic surface area under management. When tens of billions of dollars in annual spend sit inside risk-bearing arrangements for a population that historically represents one-quarter of Medicare spend, the importance of care coordination cannot be overstated.

The story is not simply that value-based care is growing. It is that kidney value-based care is integrating outward and aligning with cardiology and primary care in the process. The unit of accountability is shifting from the dialysis chair to the whole patient. But that shift raises a natural question. Is it happening in the other direction, and if so, what is driving it?

#3

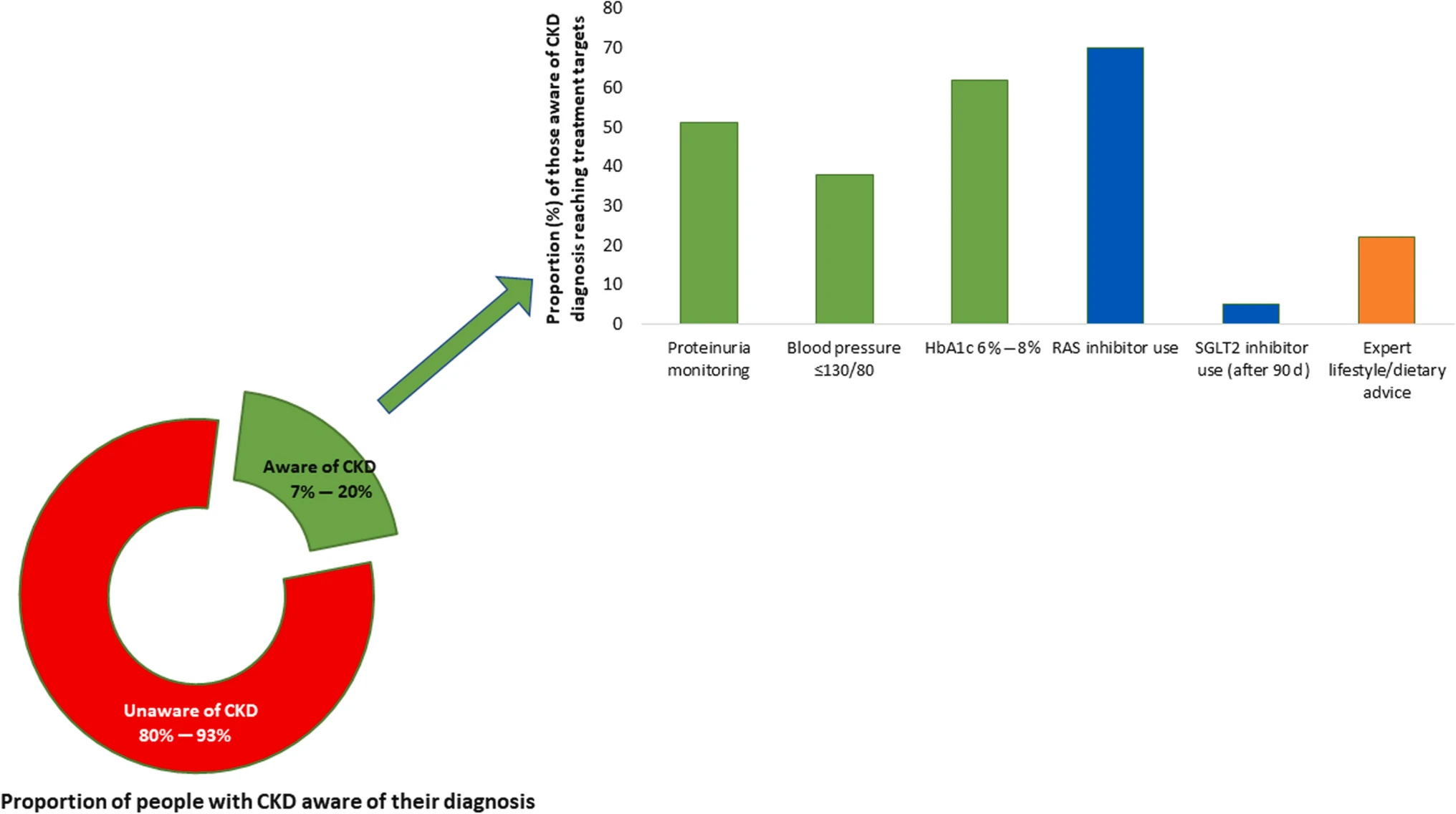

Third, primary care remains best positioned to stop kidney disease in its tracks. If CKD is going to be detected earlier and managed differently, primary care has to be center stage. It is where most patients with diabetes, hypertension, and cardiovascular disease already receive care, and where early-stage kidney risk is most likely to surface. Yet despite clear guidelines, the gap persists. The recommended tests, estimated GFR and urine albumin-to-creatinine ratio, are inexpensive, widely available, and embedded in most lab panels. They are guideline recommended for high-risk populations. Still, fewer than half of people with diabetes receive both tests, and albuminuria testing among patients with hypertension alone remains strikingly low. The tests are cheap, available, guideline recommended, and still not happening.

Figure: Proportion of people with chronic kidney disease (CKD) who are aware of their diagnosis and are receiving appropriate guideline-recommended care

Even when labs are ordered, CKD often remains invisible inside the medical record. Prior analyses suggest that nearly 80 percent of patients with moderate CKD lack a formal diagnosis in their chart. Risk is present but unmanaged, and referrals are inconsistent. The result is predictable: sixty percent of patients still initiate dialysis through an unplanned hospitalization, a moment that is clinically destabilizing and financially expensive.

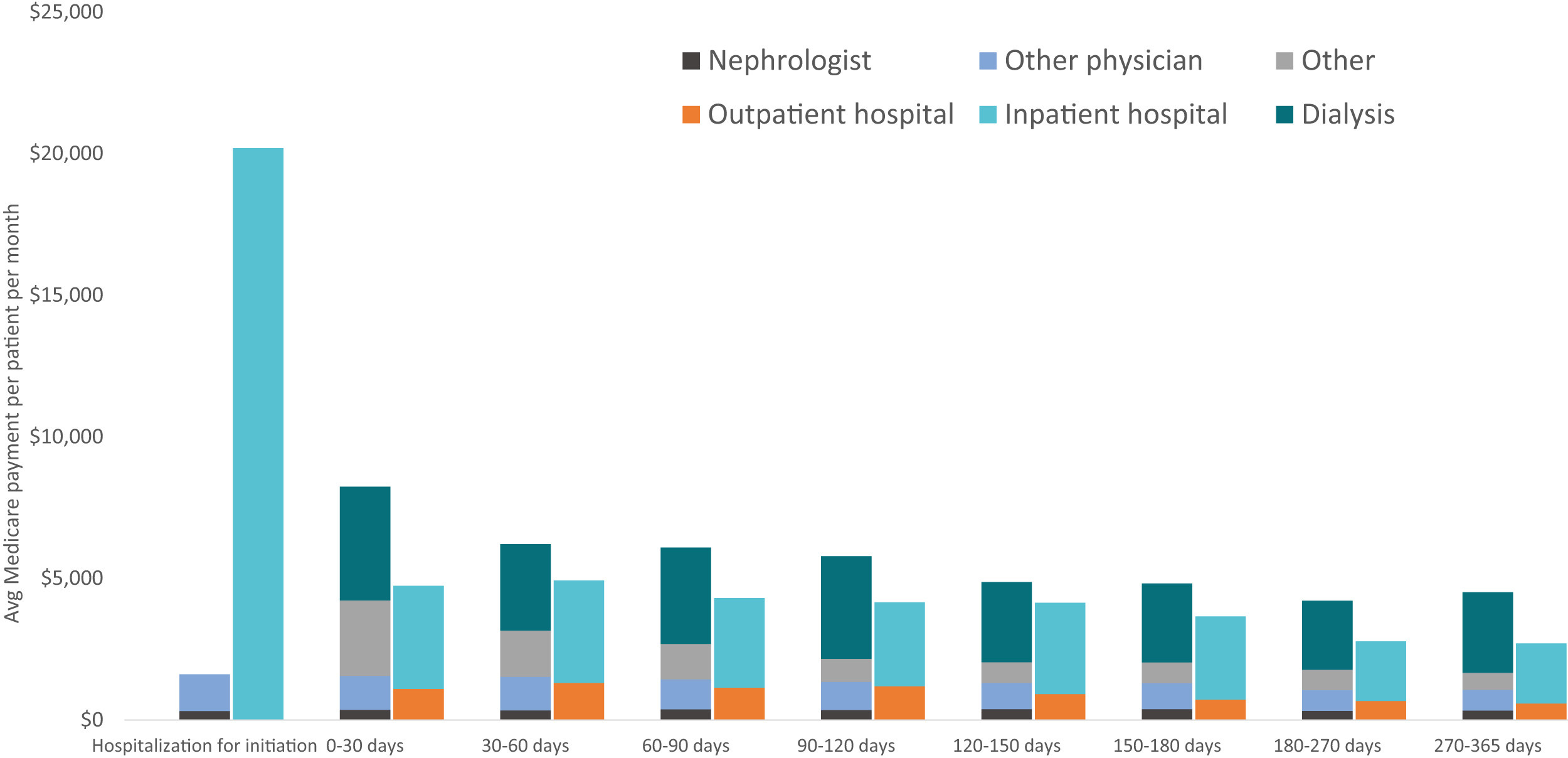

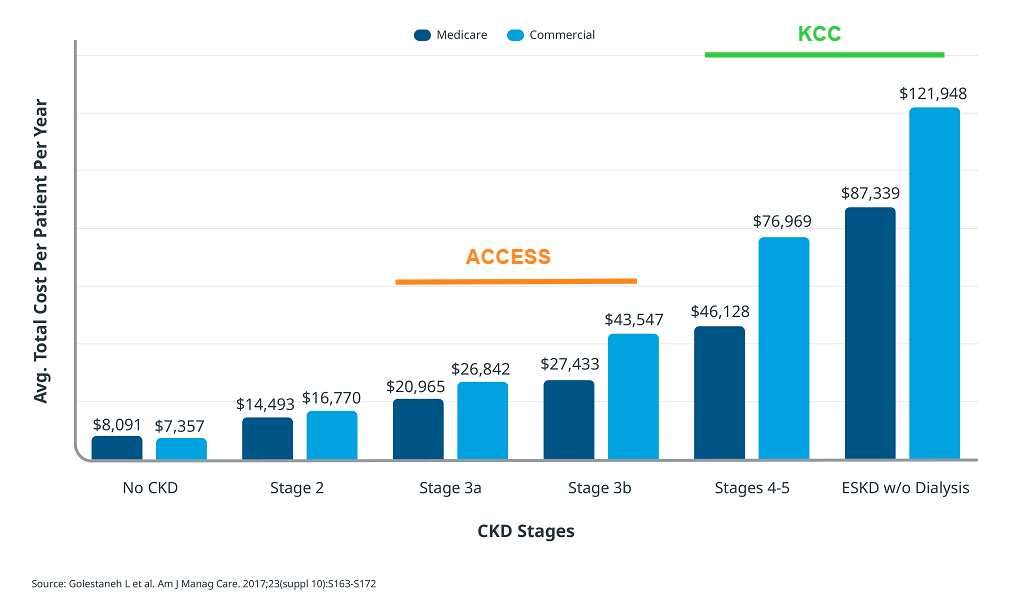

Figure: Average Medicare spending on patients initiating dialysis, 2017-2018

The economic consequences are clear. Data from Kidney Medicine show a sharp spike in inpatient hospital spending in the first 30 days of dialysis initiation, with per patient monthly costs far exceeding later periods. Federal spending on kidney failure now exceeds $50 billion annually.7 Hospitals often lose money on Medicare dialysis patients, and care remains fragmented across dialysis clinics, transplant centers, vascular access programs, and primary care. No single provider has holistic responsibility. Perhaps health systems should.

The question is whether the surrounding model makes prevention rational. In fee-for-service environments, screening and coordination can feel like friction. When a health system or primary care organization assumes responsibility for total cost of care, the equation changes. Avoiding unplanned starts, reducing hospitalizations, and coordinating specialty care move from being aspirational goals to economic imperatives. Models like ChenMed and Intermountain demonstrate how aligned incentives, embedded specialty access, and kidney-focused navigation can translate early detection into smoother transitions and fewer crisis-driven dialysis starts.

Primary care can anchor this shift, but only if it operates inside an integrated model that aligns clinical responsibility with financial accountability. That is where policy and payment design begin to matter most.

#4

Federal payment models are increasingly aligned with the clinical reality of kidney and cardiometabolic diseases. For more than a decade, CMMI has tested ways to move kidney care away from reactive dialysis spending and toward earlier, coordinated intervention. The pattern is not random. It reflects a steady recognition that late-stage payment structures produce late-stage care. If prevention is the goal, accountability has to move upstream to intervene earlier in the disease progression.8

Figure: Annual CKD Costs By Stage (2007-2012)

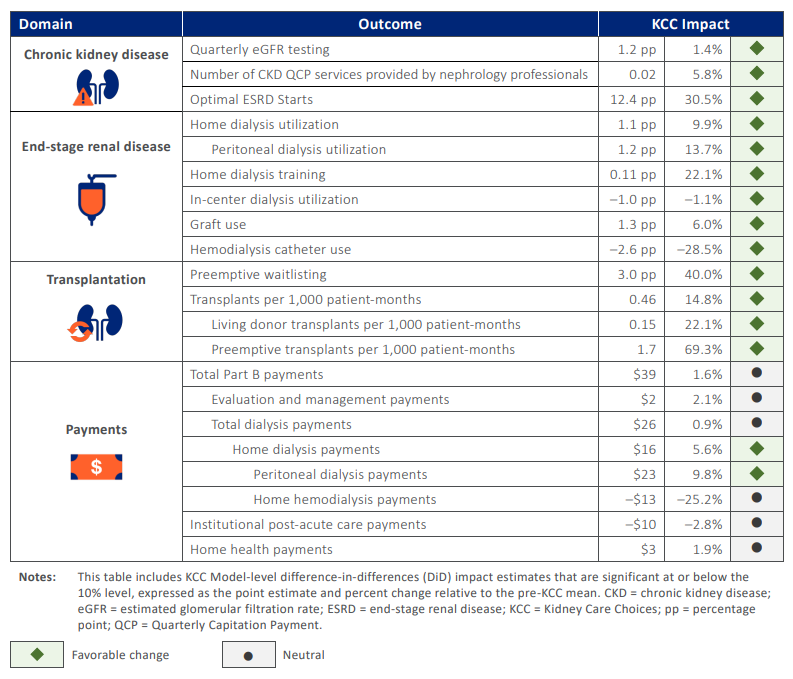

The ESRD Treatment Choices model focused on home dialysis and transplant incentives. Kidney Care Choices pushed further by bringing advanced CKD and transplant populations into risk-based arrangements. The model was extended through 2027, giving participants additional runway to translate infrastructure investments into measurable results. In its second performance year, 15 of 21 outcomes moved in a favorable direction (see below), with roughly half of eligible patients, about 225,000 people, aligned to KCC. The lesson was not that transformation is easy. It was that building care coordination, analytics, and staffing capacity requires upfront capital before downstream savings appear.9

Figure: KCC Model Outcomes, Second Performance Year (2023)

At the same time, kidney policy has been embedded inside broader accountable care structures. Chronic disease management cannot be isolated from primary care, cardiology, and population health systems. When kidney risk sits inside total cost of care arrangements, the incentives shift. Hospitalizations, unplanned dialysis starts, and transplant delays are no longer siloed specialty problems. They become financial events for the entire organization.

The next generation of models continues that evolution. ACCESS builds on kidney-specific coordination lessons by extending tech-enabled accountability earlier into CKM risk (CKD stages 3a and 3b), while LEAD introduces a ten-year accountable care pathway with improved benchmarking, population-based payments, and a focus on high-needs and dually eligible patients. A longer runway changes behavior. Organizations are more likely to invest in prevention when the contract horizon matches the biology of chronic disease. Digital tools and outcomes-aligned payments may make earlier, lower-touch interventions economically viable at scale.

Taken together, these models show that CKM is not only a clinical framework. It is becoming embedded in payment architecture. Public models often set the direction for how private payers structure risk, including Medicare Advantage and commercial plans. This broader coordination across payers is often referred to as multi-payer alignment, and it matters. When Medicare, Medicaid, and private insurers align around common measures, payment approaches, and data-sharing standards, it becomes easier for providers to invest in prevention and integrated care. When federal policy begins to price prevention, integration, and long-term accountability, the broader market tends to follow. Over time, the financial system begins to reflect the biology of chronic disease rather than react to its complications.

Note: I’m working on a piece for participants in the ACCESS model, with a few modeled scenarios for the e/CKM tracks. Please reach out if you’d like to share any insights, comments, or questions.

Forward, March

This Kidney Month, I am encouraged by how far the system has moved in the short time I’ve been paying attention.

And yet, real gaps remain. Data still struggles to move cleanly across the ecosystem: primary care, cardiology, nephrology, dialysis, and transplant. Attribution models can blur responsibility rather than clarify it. Many practices lack the physician-level tools, analytics, and care team support needed to manage CKM risk in real time. Incentives may be aligning, but operational capacity is still uneven.

These are not reasons for skepticism. They show us where to focus next. I am hopeful we will get there because of the hard work of so many of you across this ecosystem. Thank you for what you do and for helping move this progress forward.

I’d love to hear from you. What is making you optimistic right now, and what are you celebrating this Kidney Month?

This study is more to show who prescribes these drugs rather than who prescribes these drugs for CKD or ESKD in particular.